The Architecture of Resilience: Transcending the “₱200k Ceiling Trap”

In the Philippine socio-economic landscape, professional success often masks a precarious financial reality.

Most Filipino families are one illness away from the total depletion of their life savings.

This instability is driven by the Hospitalization Gap. The chasm between what modern medical care actually costs and what standard insurance provides.

While corporate (or personal) HMOs offer a perceived sense of security, they typically feature a Maximum Benefit Limit (MBL) capped between ₱50,000 and ₱500,000.

In a premier tertiary hospital, these limits are often exhausted within the first 48 hours of a critical care stay, triggering the “Abono Nightmare.”

This is the high-risk zone where insurance coverage ends and personal liability begins, often forcing families into selling assets or predatory debt.

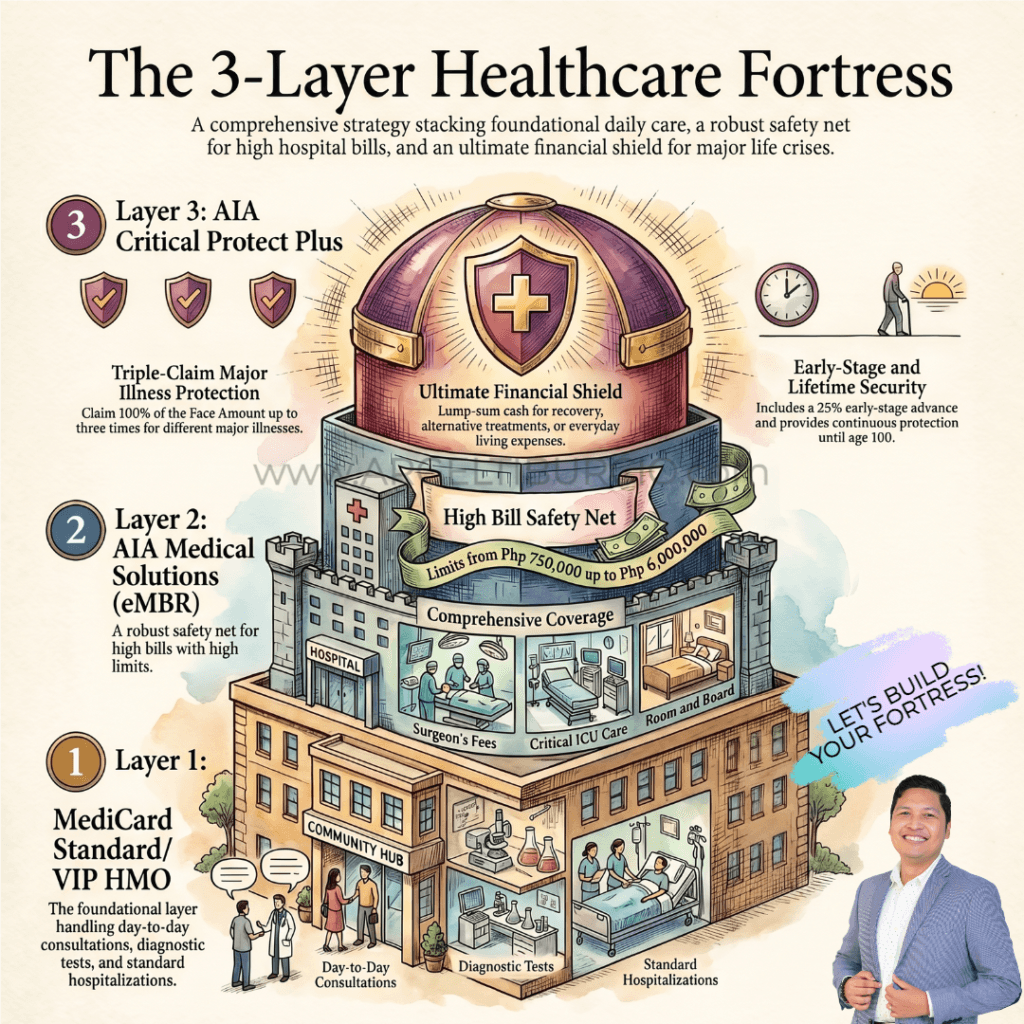

To mitigate this, Pinoys should instead construct a three-layered fortress designed to preserve financial dignity and ensure that a medical issue does not result in a financial tragedy.

Layer 1: The Foundational Perimeter (MediCard Standard/VIP HMO)

The foundation of the fortress is utilizing MediCard Standard or VIP HMO plans.

In our Healthcare Fortress, this layer serves as the “First Responder” and primary Friction Reducer.

Its strategic objective is to protect your immediate cash flow and budget from high-frequency, low-severity health events.

Benefits of Layer 1

- Preventive Care: Access to Annual Physical Examinations (APE) at MediCard Free-standing clinics to identify risks before they escalate.

- Out-patient Management: Covers regular consultations and diagnostics to ensure early intervention.

- The “No Deposit” Feature: This is a critical tactical advantage. Upon admission to accredited hospitals, your MediCard HMO status eliminates the need for immediate cash deposits, ensuring medical attention is not delayed by bank transfer limits.

The “So What?” Factor: Layer 1 is designed to handle the “medical noise” such as fevers, lab tests, and minor ER visits. It ensures that the family’s daily operational funds remain untouched.

However, Layer 1 is critically insufficient for catastrophic diagnoses. Relying on it alone leaves the fortress gate wide open for million-peso hospital bills.

Layer 2: The Catastrophic Buffer (AIA Medical Solutions with eMBR)

To bridge the Hospitalization Gap, we deploy the Catastrophic Buffer.

This utilizes the Enhanced Medical Benefit Rider (eMBR), acting as a “High-Limit Bridge” that standardizes care across the Philippines’ top-tier facilities (e.g., St. Luke’s, Makati Med).

This layer takes over the heavy lifting exactly where the primary HMO fails.

eMBR Strategic Configuration (Aggregate Limits)

Benefit | Plan A | Plan B | Plan C | Plan D |

|---|---|---|---|---|

Max Coverage / Year | ₱750,000 | ₱1,500,000 | ₱3,000,000 | ₱6,000,000 |

Room & Board (Daily) | ₱1,000 | ₱2,000 | ₱4,000 | ₱8,000 |

ICU / Critical Care | ₱2,000 | ₱4,000 | ₱8,000 | ₱16,000 |

Surgeon’s Fee Limit | ₱20,000 | ₱40,000 | ₱80,000 | ₱160,000 |

Risk-Sharing (Co-Payment Ratios)

Take note that you must account for very minimal out-of-pocket friction. The eMBR operates on a co-share model after PhilHealth:

- Within-Network (Non-PEC): 90:10 Ratio.

- Within-Network (Pre-Existing/PEC): 80:20 Ratio (after a 12-month waiting period).

- Outside-Network (PEC): 70:30 Ratio.

The “So What?” Factor: Layer 2 mitigates “Sequence of Returns Risk.”

It ensures that a major medical bill does not force you to sell stocks or real estate during a market downturn. By erasing the hospital bill, it preserves your investment timeline. However, while the bill is erased, your income often stops, hence the need for the final shield.

Watch the benefits of aia medical solutions below:

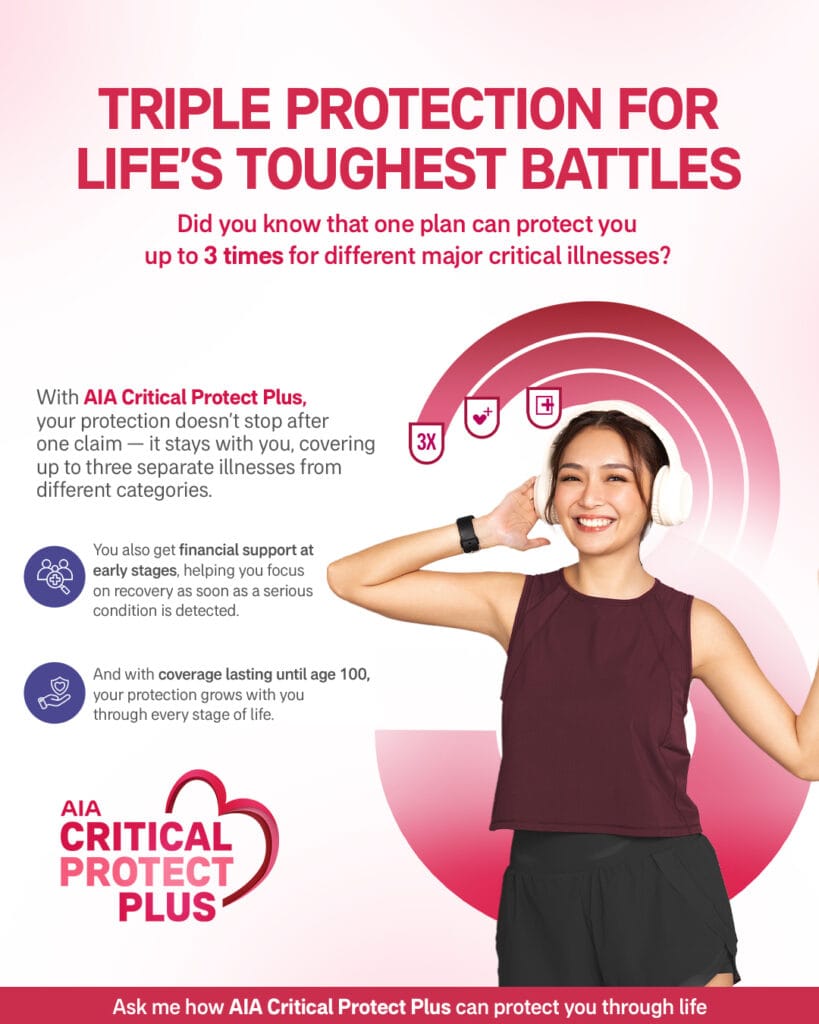

Layer 3: The Strategic Income Shield (AIA Critical Protect Plus)

The topmost layer is the Strategic Income Shield (ACPP). This is a unique “Recovery Fund” because it pays you, not the hospital.

While Layers 1 and 2 are for the Hospital, Layer 3 is for your Lifestyle Continuity.

Core Benefits:

- Triple-Claim Multi-Stage Protection: Allows for three separate Major Critical Illness claims (100% of Face Amount each) across five distinct illness groups.

- Early-Stage Advance: Provides a 25% advance (up to ₱1M) for minor conditions.

- Exception: Claims for Early Thyroid Cancer are specifically capped at 10% of the Face Amount or ₱1M, whichever is lower.

- Waiver of Premium: Upon the first major claim, all future premiums for the base plan and riders are waived, maintaining the fortress for free.

- Whole Life Coverage: Protection remains in force until age 100, securing wealth for the family even in the absence of a claim.

The “So What?” Factor: Medical recovery is a hiatus from productivity. Without a lump-sum cash drop, a family’s lifestyle (mortgages, tuition, and utilities) collapses during the rehabilitation phase.

Layer 3 preserves the family’s standard of living, allowing the breadwinner to focus on healing without financial shame.

Value-Added Optional Benefits: Riders and Wellness Integration

Optional riders allow for a bespoke configuration of your fortress based on specific vulnerabilities.

- Gender-Specific Cancer Benefit: Provides an additional 25% payout for targeted recovery (e.g., breast/cervical for women; prostate/testis for men).

- Critical Care Assist: Provides 10% of the Face Amount (up to ₱500k) specifically if the insured is in the ICU for 5+ consecutive days following major surgery on vital organs (Heart, Brain, Lungs, Liver, or Kidneys) requiring life support.

- Emerging Conditions Benefit: Coverage for “pre-critical” issues like benign tumors or thyroid disorders (10% payout, up to ₱500k).

- AIA Vitality: A “reset model” where healthy habits lead to a 20% to 50% coverage boost on eligible riders, rewarding the client for proactive health management.

The “So What?” Factor: These riders transform a generic policy into a precision-engineered solution. For high-risk Pinoys, they ensure the fortress is reinforced exactly where it is most likely to be tested.

Case Study: The Fortress in Action

Scenario: A 45-year-old breadwinner suffers a severe heart attack requiring major surgery and 10 days in the ICU.

- Total Bill: ₱1,500,000

- Income Loss (6 months): ₱2,000,000

The Activation Sequence:

- Layer 1 (MediCard): Takes the first ₱150,000 (ER and initial testing).

- Layer 2 (AIA eMBR): Covers the ₱1,350,000 balance. Under the 90:10 co-pay for non-PEC, the plan pays ₱1,215,000 to the hospital. The client’s remaining 10% friction is ₱135,000.

- Layer 3 (AIA Critical Protect Plus): Upon diagnosis, a ₱2,000,000 lump sum is deposited into the client’s bank account.

- Strategic Result: The ₱2M cash drop “mops up” the ₱135,000 co-pay instantly, leaving ₱1,865,000 for income replacement. Savings remain intact, and all future premiums are waived.

Stop being lucky and start being ready.

The difference between a medical miracle and a financial catastrophe is the architecture of your defense.

Message me today to identify your Hospitalization Gap before the crisis arrives.