The Cost of Delaying Investing

As a Financial Adviser, I have no control whether or not my client who I personally meet for a 1-on-1 Financial Planning session will start right away with investing for his or her financial goals.

I’m cool with that because what I can control is to give my full-out effort during the meeting in order to let my clients realize what’s best for them.

During my presentations, I make sure that I provide urgency especially for my clients who have lots of big financial goals but haven’t started any “real” investing yet. (I’m sorry to tell you but “saving” in the bank is not “investing”)

One of my tasks as a Financial Adviser and Financial Planner is to determine how much would my client need to set aside and invest in order to save for a specific financial goal.

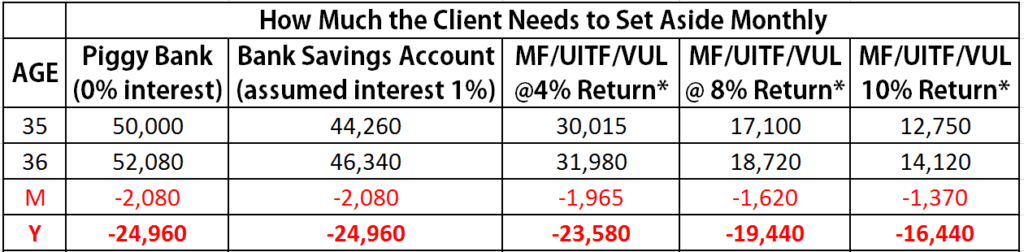

Let’s say, my client who’s 35, wants to retire at age 60 with a target Retirement Fund of PhP15,000,000

If the client decides to invest as soon as possible:

Let’s break it down.

If the client does not want to invest and just want to save in the piggy bank for the next 25 years, the client needs to set aside PhP50,000 per month.

If the client chooses to save in the bank (with an assumed yearly interest rate of 1%), the client needs to save a little bit less, PhP44,260, compared to the piggy bank.

Here comes the power of investing:

If the client decides to invest in a Mutual Fund (MF), Unit Investment Trust Fund (UITF) or Variable Unit-linked insurance (VUL), the client will set aside even lesser.

This will save money for the client. Instead of setting aside a whopping 50,000 pesos, he or she can invest only around 13,000 – 30,000 pesos!

However…

Not all clients are “ready” when I meet them. Sometimes, they choose to spend on short-term expenses like cars, condominiums, travels or gadgets while some are buried in debt.

To drive my point, I will show how much a client may lose if they choose to delay investing for their financial goal for one (1) year.

The red “M” row is the monthly cost of delaying investing for a single year.

The red “Y” row is the total cost of delaying for a year.

That’s the difference that one year of delaying investing can make. What if they choose to delay for two years? Five years? Ten years?

These amounts could have been used by the client elsewhere. These could have been used to purchase the gadget or even add to the travel budget that a client wants.

Do you agree?

To conclude, the biggest cost of investing is the cost of delaying.

If you want to stop delaying and start investing, contact me now.

Comment your insights and realizations below.

Share this with your friends or relatives who want to “think over” their decisions but they never take action anyway.

To our success in all areas of life,

Argel Tiburcio, CIS

I’m on Facebook: http://fb.com/ArgelTiburcioPFA