What is Life Insurance?

Now that we already know the types of risk, let’s focus on one risk that most people don’t even think about: the risk of losing their life.

Actually, I do not want to sound morbid but losing our life is 100% guaranteed to happen.

Everybody dies.

What we don’t know is when it would happen.

Correct? Say “Yes!”

Since we are in the context of personal finance, our major concern when we lose our lives is that we also lose our capacity to earn.

Especially when we have people depending on our income.

Primarily, these people are our family.

They depend on our income so that they can have their most basic needs: food, shelter, clothing, security.

That said, we would want our family to survive even if we already left this world.

And that’s when Life Insurance comes in.

Investopedia defines Life Insurance as:

A protection against the loss of income that would result if the insured passed away. The named beneficiary receives the proceeds and is thereby safeguarded from the financial impact of the death of the insured.

Nice definition right?

But how come for most people, life insurance is not part of their plan?

That’s because most people lack the proper financial education.

They think the life insurance is a waste of money.

But if they think of it as a way to lessen the family’s problem when they suddenly pass away, then they would realize how important life insurance is.

Another thing that affects their decisions is the cost of life insurance.

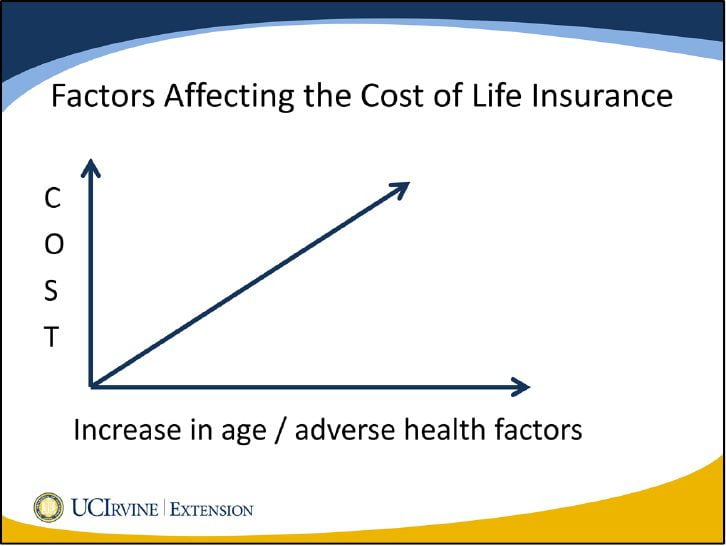

Below is a very simple graph from coursera.org showing the relationship between the cost of life insurance and time & health factors:

In a nut shell, the older we get, the higher the cost of life insurance.

Aside from that, health factors also affect the cost of life insurance.

These include: personal health history, tobacco use, alcohol use, family health history, and even gender.

So don’t think that insurance providers are tricking you and giving you amounts that are just invented out of thin air.

I believe that there is also some kind of baseline for the pricing.

Insurance companies may have an acceptable difference for their same line of life insurance products.

Types of Life Insurance

We can classify the types of life insurance in the Philippines into three broad categories, Permanent (or Whole Life), Term and Variable Unit-Linked.

1. Permanent Life Insurance

Investopedia defines Permanent Life Insurance as:

An umbrella term for life insurance plans that do not expire (unlike term life insurance) and combine a death benefit with a savings portion. This savings portion can build a cash value – against which the policy owner can borrow funds, or in some instances, the owner can withdraw the cash value to help meet future goals, such as paying for a child’s college education.

2. Term Life Insurance

Again from Investopedia:

A policy with a set duration limit on the coverage period. Once the policy is expired, it is up to the policy owner to decide whether to renew the term life insurance policy or to let the coverage end. This type of insurance policy contrasts with permanent life insurance, in which duration extends until the policy owner reaches 100 years of age (i.e. death).

I just want to emphasize that there is no silver bullet when it comes to the type of insurance that you would like.

It all boils down to the financial goals that we might have.

Do you want to cover just a certain segment of your life? Then, opt for term life insurance.

Do you want to make sure you are covered until you are 98 years old? Opt for permanent life insurance.

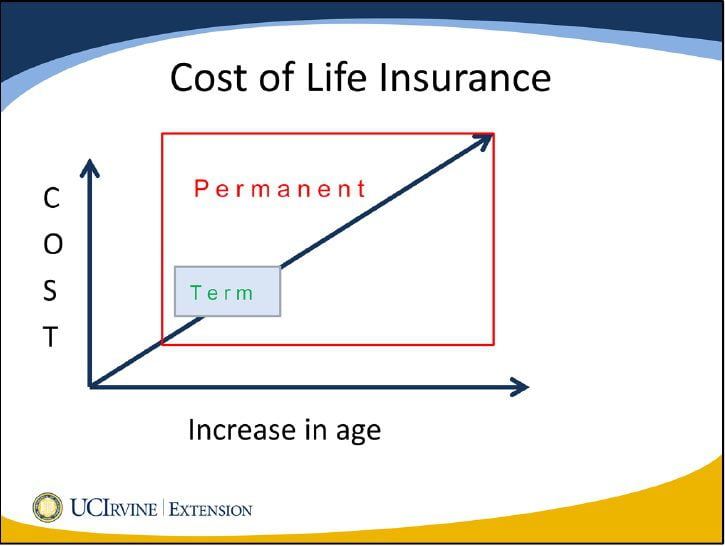

I would like to borrow again from coursera.org so that you can visualize the difference between Term Life Insurance and Permanent Life Insurance:

With this, you can see the main differences of the two broad categories of life insurance in terms of cost and time.

Term life insurance protects you within a short period of time but it is significantly lower in cost as compared to permanent life insurance.

Now, you might ask me what type of life insurance I have.

3. Variable Unit-Linked Insurance

The type of life insurance I own combines mutual funds and insurance in one!

Plus, I am protected until age 100!

If I don’t prematurely die, I can use the mutual fund earnings as my Retirement Fund. Also, I can accelerate the growth of my retirement fund by topping-up additional savings to the mutual fund.

It also has additional benefits for disability and critical illnesses so that I won’t get from my savings or investments if ever I get diagnosed with life-threatening illnesses like cancer, heart attack or stroke.

I hope you had a general sense of what life insurance is all about.

If you have questions or clarifications, simply leave a comment below.

Until then.

To our success in all areas of life,

Argel Tiburcio, CIS, RFP Graduate Member

I’m on Facebook: http://fb.com/ArgelTiburcio

Image Source: http://www.flickr.com/photos/dhilowitz/4560586060/

Indeed, life insurance certainly plays an important role in society of protecting the welfare of individuals and families but sometimes we do take these things for granted don’t we? but we would be in a heck of a mess without them! well done!

Yup, you’re right, we do take insurance for granted. Thanks for your insights, Connie!